Supply & Demand: Short Domain Names Investment Case Study Nov 2 2007 Buyout

Supply & Demand: Short Domain Names Investment Case Study Nov 2 2007 Buyout

Money and business are moving into the virtual world. Traditional industries are mature and markets are efficient there — which means the margins are thinner and competition is fiercer. Wealth is gradually shifting toward digital assets, and understanding how to evaluate these opportunities requires going back to basics: supply and demand.

This video walks through the economics of short .com domain names using the November 2, 2007 four-letter .com buyout as a concrete case study.

The Physical-Digital Parallel

Think about property. At the top of the market, a trophy building like the Bank of America Tower costs a fortune. The digital equivalent — a one-word .com like insurance.com or hotels.com — demands the same kind of capital. Most investors cannot participate at that level.

The actionable opportunity is one tier down. In physical real estate, that means a residential property or small commercial space. In the digital world, it means a four-letter .com domain. These are assets an individual can actually acquire and hold.

The rules governing value in both worlds share a common logic. Physical property follows the mantra of location, location, location. Domain property follows the mantra of short, shorter, shortest. And just as no one should buy a house in the middle of a desert with no roads, no one should invest in domains with hyphens or numbers. Those names lack the fundamental characteristics — memorability, typeability, brandability — that drive value.

Counting the Supply

Four-letter .com domains are governed by a hard mathematical limit. With 26 possible letters in each of four positions, there are exactly 456,976 possible combinations. For three-letter .coms, the ceiling is 17,576. These numbers can never increase. Unlike physical real estate, where new land can occasionally be reclaimed or rezoned, the namespace is permanently fixed at creation.

Each domain sits in one of three buckets at any point in time: unregistered (available for the standard registration fee), held by a domain investor, or held by an end user running a business on it. The movement between these buckets flows in one direction. End users buy from investors. Investors register what is freely available. The unregistered pool shrinks over time, and names that end up powering active businesses rarely come back to market.

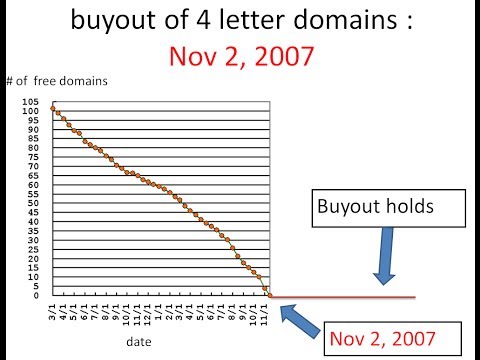

What Happened on November 2, 2007

That date marked the moment when every single four-letter .com combination was registered. The count of freely available names dropped to zero. The chart tells the story — a gradual decline over months, accelerating into a steep drop as investors rushed to grab the final available combinations, and then the line flatlines at zero.

Before that date, anyone could register a four-letter .com for roughly $10. After it, every acquisition required buying from an existing owner at market price. The shift was permanent. If you had purchased domains before the buyout, you were positioned on the right side of a supply squeeze that has held for nearly two decades.

Even after November 2, opportunity existed. Many market participants doubted the buyout would stick — they expected names to expire, drop back to the available pool, and push prices down. That skepticism kept prices lower than the fundamentals justified and created a window for informed buyers.

How Letter Quality Affects Price

The 26 letters of the English alphabet are not equally valuable in domain names. Experienced investors sort them into tiers based on how frequently they appear in words and how easily they combine into pronounceable, memorable strings.

Premium letters — the ones that show up most often in common English — are the most sought-after. Letters like Q, X, Z, and J sit at the bottom. A middle group falls in between. This ranking system might remind you of Scrabble tile values, but domain letter frequency is its own distribution based on commercial naming patterns, not just word frequency.

The practical impact is significant. A four-letter domain composed entirely of premium letters — something that sounds like it could be a brand name — commands a substantial premium over a random string with low-frequency characters. Paying more for better letters is not overspending; it is buying the quality tier that has real commercial demand from end users.

Watching the Market Move: Prices Before and After the Buyout

Historical auction data from the period around the buyout provides a clear picture of how sentiment and price interacted.

About a year before the buyout, premium-letter four-letter .coms were changing hands at roughly $60. This was well below their eventual value, but the market had not yet priced in the coming supply squeeze. Even with the available pool visibly shrinking, most buyers remained cautious.

Whenever a batch of domains dropped (expired registrations that re-entered the pool), confidence dipped. People saw available names and assumed the scarcity story was overstated. This pattern persisted until just a few months before the buyout.

September 2007 was the inflection point. Prices jumped to $100 and above, though bargains still appeared sporadically. October brought the land rush — buyers scrambling to lock in positions before the final names disappeared. By the buyout date itself, premium-letter combinations were trading near $200.

The spike did not hold at that level. By 2008 — compounded by the global financial crisis — prices settled around $170 for premium names. Domains with mixed-tier letters (say, three good letters and one mid-range) were trading around $59.

Building an Edge Through Data

The single most important practice in domain investing is studying auction data systematically. Raw auction results — buyer usernames, winning bids, domain names, dates — go into a spreadsheet or database. Sort by buyer, and patterns emerge. Certain accounts consistently win bids on premium names. These are the informed players, and understanding their behavior tells you where the money sees value.

This analysis has a second benefit beyond market intelligence. By identifying active buyers in your market segment, you can reach out, compare notes, and eventually build real relationships. Two of my own competitors became real-life friends through exactly this process. Having a support network of people who understand the market is valuable beyond the data itself — especially during periods when prices dip and doubt sets in. Without that network, it is easy to lose confidence and sell prematurely.

The cardinal rule of buying is to never purchase a domain because you personally like it. You are not the customer. The question is always whether someone else will want it — whether demand exists beyond your own preference. Data answers that question. Instinct does not.

Two Types of Sales

Domain sales happen in two distinct markets with very different economics.

Selling to another domainer is quick but low-margin. Professional investors are well-informed, so the spread between buy and sell prices is narrow. The market is efficient. Most serious portfolio holders avoid domainer-to-domainer flipping except as a short-term tactic.

Selling to an end user — a company that actually wants the domain for its brand — is where the returns are. This market is inefficient, meaning the gap between what you paid and what a motivated business will pay can be enormous. The catch is timing. One domain might take 20 years to find its end-user buyer. A portfolio of 20 domains might generate one end-user sale per year on a statistical basis. The math works, but only with patience and sufficient portfolio size.

Legal Protection for Domain Owners

One concern for domain investors is the possibility of a trademark holder attempting to take a domain through the UDRP (Uniform Domain-Name Dispute-Resolution Policy). A UDRP filing costs around $1,500, but the complainant must demonstrate three things: that the domain is identical or confusingly similar to their mark, that the registrant has no legitimate interest, and that the domain was registered and used in bad faith. All three must hold.

This standard protects investors. Owning a generic four-letter combination is not bad faith, and legitimate investment constitutes a recognized interest under the policy.

When a trademark holder files a UDRP they know they cannot win — hoping to bully the registrant into surrendering the name — the panel can issue a finding of reverse domain name hijacking. This goes on the complainant’s record and acts as a deterrent. It is a tool every domain investor should know about.

The Risk Side

No investment is without risk. The biggest question mark for domain investors is the proliferation of new top-level domains. When only .com, .net, and .org existed, the value proposition of a short .com was straightforward. Now there are hundreds of alternatives — .io, .ai, .xyz, .app, and custom TLDs for every industry imaginable.

Has this diluted the value of .com? So far, the evidence says no — .com remains the default and premium short .coms have continued to appreciate. But the question is worth asking, and each investor must assess the risk according to their own analysis.

Other risks include changes in how people navigate the internet (voice search, app-based ecosystems, social media handles as primary identifiers) and regulatory changes to domain governance. None of these have materially impacted short .com values to date, but the landscape continues to evolve.

The Bottom Line

This case study is not investment advice. It is an exercise in applying economic fundamentals to a specific asset class. The supply of four-letter .com domains is permanently capped at 456,976. Demand from businesses needing online identities grows every year. The November 2, 2007 buyout demonstrated what happens when available supply hits zero against growing demand — and that dynamic has not reversed.

For more technology and investment perspectives, see our articles on internet access tips for travelers and Amazon Web Services introduction.